ISC Accountancy Specimen Paper 2023-2024 for Class 12: Council for the Indian School Certificate Examinations (CISCE), the official education board for all ISC and ICSE schools has released its Specimen Paper for the current academic session 2023-2024. Students preparing for upcoming ISC Board Examinations 2024, must have a look at these specimen papers for all subjects of Class 12 before they take a step further in their academic journey.

Specimen Papers, also known as Sample Papers are a blueprint of your final question paper. It consists of general instructions present in the question paper, types of questions, pattern of questions, number of questions, and marks allotted to each question. Basically, it is the exact replica of the question paper pattern that you would be getting for your final examinations. Thus, it plays a crucial role in your preparation for board examinations.

How to download Specimen Paper 2024 for ISC Class 12 Accountancy?

Follow the below-mentioned steps for easy download of ISC Class 12 Accountancy Specimen Paper 2024:

- Go to CISCE’s official website, cisce.org.

- You can find an ‘Examination’ option, on the top bar. Click on it.

- A dropdown box will appear, containing options for choosing between the ICSE and ISC examinations. Click on ISC Examination.

- Scroll down the page to find ‘Important Downloads’.

- Click on ‘Specimen Question Papers

- Go to ‘Specimen Question Papers ISC- Class XII and scroll down to click on 2024

- Now, scroll down until you find an option for Accountancy

- Click on it and download the PDF using the downward arrow sign present at the top.

ISC Class 12 Accountancy Exam Pattern 2024

Find the ISC Class 12 Accoutancy exam pattern 2024 below in a few points. Check the question paper pattern and know about the upcoming question paper in detail.

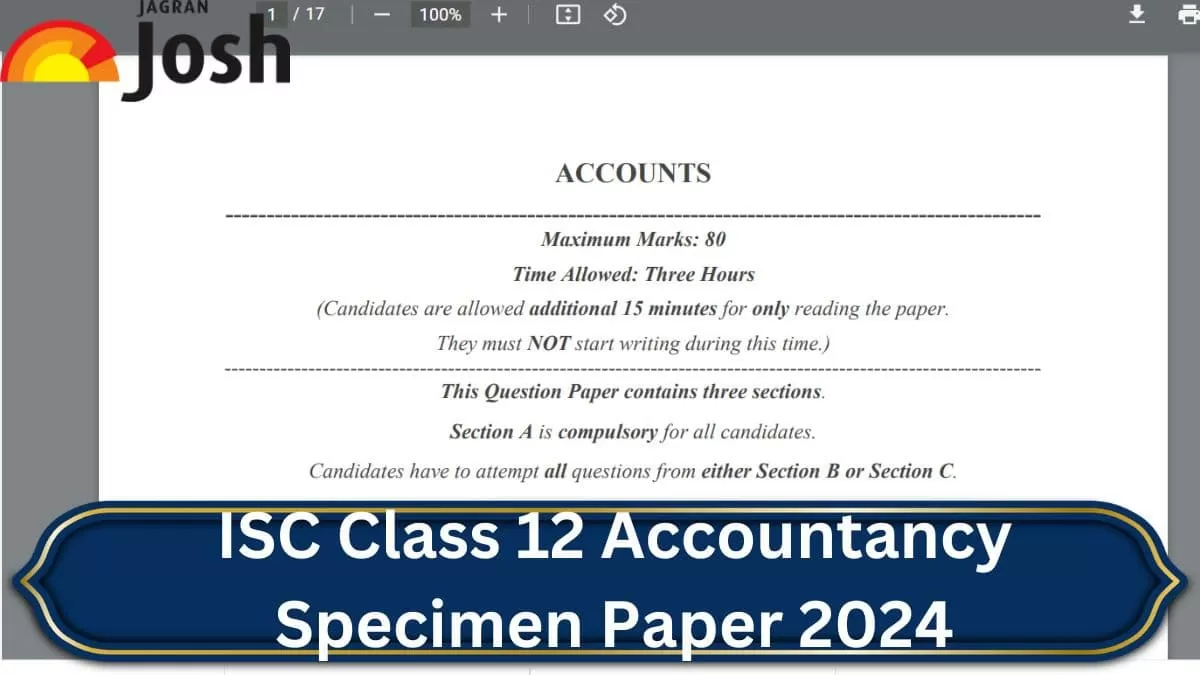

General Instruction for ISC Class 12 Accountancy Board Examinations (as per ISC Class 12 Accountancy Specimen paper 2024)

- This Question Paper contains three sections.

- Section A is compulsory for all candidates.

- Candidates have to attempt all questions from either Section B or Section C.

- There are internal choices provided in each section.

- The intended marks for questions or parts of questions are given in the brackets [].

- All calculations should be shown clearly.

- All work, including rough work, should be done on the same page as, and adjacent to, the rest of the answer.

ISC Class 12 Accountancy Specimen Paper 2024

Question 1

In subparts (i) to (iv) choose the correct options and in subparts (v) to (x) answer the questions as instructed.

(I) On the date of Som’s admission as a partner, it is decided that:

- Furniture (book value ₹ 2,50,000) be reduced by 40%

- Machinery (book value ₹ 1,50,000) be reduced to 40%.

What is the net decrease in the value of the assets?

(a) ₹ 2,10,000

(b) ₹ 1,90,000

(c) ₹ 1,60,000

(d) ₹ 2,40,000

(ii) Anita, Benu and Chitra dissolve their partnership firm. Anita had taken a loan of ₹ 10,000 from the firm. What will be the entry to settle Anita’s Loan on the dissolution of the firm?

(a) Debit Realisation A/c; Credit Anita’s Loan A/c

(b) Debit Anita’s Loan A/c; Credit Realisation A/c

(c) Debit Anita’s Capital A/c; Credit Anita’s Loan A/c

(d) Debit Bank A/c; Credit Anita’s Loan A/c

(iii) A company issued 5,000, 10% Debentures of ₹ 100 each at a discount of 5%. To write off the capital loss, it has to use its profits in a certain order. Chose the correct order in which the profits are used by the company to write off the capital loss: Statement of Profit & Loss Q Capital Reserve R Securities Premium

(a) P, Q, R

(b) R, P, Q

(c) R, Q, P

(d) Q, P, R

(iv) The Subscribed Capital of a company refers to:

(a) The paid-up value of the shares allotted on the date of the balance sheet.

(b) The called-up value of all shares allotted on the date of the balance sheet.

(c) The nominal value of all shares allotted on the date of the balance sheet.

(d) The paid-up value of all shares allotted on the date of the balance sheet and the balance of shares forfeited account, if any.

(v)Jia, Tia, Sia and Bashir are partners sharing profits in the ratio of 3:3:2:1. Tia retires from the firm. Bashir retains his original share in the reconstituted firm. Jia takes over 2 3 ⁄ of Tia’s share and the balance is taken up by Sia. What is the new profit-sharing ratio of the remaining partners in the reconstituted firm?

(vi)Assertion : Goodwill is a fictitious asset.

Reason : Goodwill has a realisable value. Which one of the following is correct?

(a) Both Assertion and Reason are correct, and Reason is the correct explanation for Assertion.

(b) Both Assertion and Reason are correct, but Reason is not the correct explanation for Assertion.

(c) Assertion is false and Reason is true.

(d) Assertion is true and Reason is false.

(vii) At the time of dissolution of a partnership firm, its Balance Sheet showed stock of ₹ 40,000 comprising of easily marketable items, obsolete items, and a few miscellaneous other items. These items were realised as:

- Easily marketable items: 70% of the total inventory - in full.

- Obsolete items: 10% of the remaining inventory - discarded.

- The miscellaneous other items in the stock - 20% of their book value.

You are required to calculate the amount realised from the sale of stock.

(viii) As a result of the measure taken by the government in the year 2019-20 of non-creation of Debenture Redemption Reserve by listed companies / NBFCs or HFCs, the investments in the debenture issues from these companies have become riskier. Source (edited): The Hindu, August, 2019 State the adverse impact of this measure on the investors?

(ix) Give any one difference between a company’s balance sheet and a firm’s balance sheet.

(x) Matrix Ltd. (an unlisted construction company) redeems its 7,000, 10% Debentures of ₹ 100 each in instalments as follows:

Date of Redemption Debentures to be redeemed

31st March, 2022 2,000

31st March, 2023 3,000

31st March, 2024 2,000

How much will the company transfer from Debenture Redemption Reserve to General Reserve on 31st March, 2023?

Question 2

On 31st March, 2023, Parul retired from active partnership and her share of the following was ascertained on the date of her retirement:

Particulars (₹)

Goodwill 20,000

Interest on Capital 2,000

Drawings 19,000

Interest on Drawings 3,000

Share of Profit 30,000

Capital 70,000

The amount due to Parul was kept with the firm as a loan, bearing interest @ 6% per annum. It was to be paid in two equal annual installments along with interest @ 6 % per annum, the first installment being paid on 31st March, 2024. You are required to prepare Parul’s Loan Account until the payment of the whole amount due to her is made.

OR

Piu and Nina are partners in a firm sharing profits and losses in the ratio of 3:1 respectively. Nina retires and her claim, including her capital and entitlements from the firm including her share of goodwill of the firm, is ₹ 60,000. After this amount was determined, it was found that there was some unrecorded office equipment valued at ₹ 18,000 which had to be recorded. Upon recording this office equipment, the revised amount due to Nina was determined and Piu settled it by giving Nina this office equipment and for the balance she drew a promissory note. You are required to give the necessary journal entries to record the transactions on the date of Nina’s retirement.

Question 3

On 1st April, 2021, Kant Ltd. issued 8,000, 12% Debentures of ₹ 100 each, redeemable at par after five years. The issue was fully subscribed. According to the terms of the issue, interest on debentures is payable annually on 31st March. Tax deducted at source is 20%. You are required to pass journal entries to record the transactions of interest on debentures only for the year 2022-23.

Question 4

Leo Ltd. (a listed NBFC) redeems its 9,000, 10% Debentures of ₹ 100 each at a premium of 5 % in installments, as follows:

Date of Redemption Debentures to be redeemed

31st March, 2021 2,000

31st March, 2022 2,000

31st March, 2023 5,000

You are required to prepare:

- The Debenture Redemption Investment Account for the years 2021-22 and 2022-23.

- 10% Debentures Account for the year 2021-22.

OR

Honesty Ltd., an unlisted manufacturing company, had 30,000, 6% Debentures of ₹ 100 each due for redemption at par on 31st March, 2023. On this date the company had the required amount of ₹ 3,00,000 in its Debenture Redemption Reserve. The Debenture Redemption Investment, which was purchased on 30th April, 2022, was realized at 101% on the date of redemption of the debentures and the debentures were redeemed. You are required to pass journal entries in the books of the company for the year 2022-23. (Ignore interest on debentures)

Question 5

From the information given below, find the average profits of the partnership firm of Sudhir and Sana.

(a) The firm has total assets of ₹ 4,80,000.

(b) The partners’ capital accounts show a balance of ₹ 4,00,000.

(c) The firm has reserves of ₹ 30,000 and creditors of ₹ 50,000.

(d) The normal rate of return from the capital invested in the same class of business is 10%.

(e) The self-generated goodwill of the firm is valued at ₹ 1,80,000 at 3 years’ purchase of super profits.

Question 6

On 1st April, 2021, Vintage Ltd. was registered with a capital of ₹ 40,00,000 divided into equity shares of ₹ 100 each. It offered 12,000 shares to the public which were all subscribed for and allotted and were fully paid. During the year 2022-23, the company:

- Issued 5,500 equity shares to the public on which, till the date of the Balance Sheet as at 31st March, 2023, ₹ 70 had been called.

- Issued equity shares of ₹ 100 each at a premium of ₹ 25 to Style Ltd. from whom it purchased land at a purchase consideration of ₹ 4,50,000.

- Paid underwriting commission of ₹ 40,000 to the underwriters.

- Suffered a net loss of ₹ 4,00,000.

As per Schedule III of the Companies Act, 2013, you are required to:

(a) Show the Reserves and Surplus in the Notes to Accounts.

(b) Mention the heading and sub-heading under which Land is shown in the Balance Sheet of the company.

(c) Give the amount of Share Capital in the Balance Sheet of the company prepared as at 31st March, 2023. (Ignore Notes to Accounts)

Question 7

Sharan and Angad are partners in a firm sharing profits and losses in the ratio of 3:2. On 1st April, 2022, they admit Akhil as a partner for 1 5 ⁄ share in the profits. Akhil acquires 1 5 ⁄ of his share from Sharan and the balance from Angad. On the date of Akhil’s admission, the goodwill of the firm was valued at ₹ 90,000. Akhil contributed the following assets towards his capital and his share of goodwill.

Particulars (₹)

Cash 60,000

Debtors (less provision for doubtful debts) 20,000

Land and Building 1,00,000

Plant and Machinery 80,000

You are required to:

(a) Calculate the sacrificing ratio of the partners

(b) Pass the necessary journal entries on Akhil’s admission, ascertaining Akhil’s capital contribution and assuming that he brings into the firm his share of goodwill in cash/ kind.

OR

Amit and Pavan are partners in a firm with capitals of ₹ 35,000 each. They shared profits and losses in the ratio of 3:1. On 1st April, 2023, they admit Charu as a new partner for 1 5 ⁄ share in the profits. Charu brings in ₹ 40,000 as her share of capital. Goodwill of the firm is based on Charu’s share in the profits and the capital contributed by her. Charu brings her share of goodwill in cash. At the time of Charu’s admission:

- The firm had a General Reserve of ₹ 60,000 from which ₹ 20,000 is to be set aside as provision for doubtful debts.

- Creditors of ₹ 8,000 are paid by Amit privately for which he is not to be reimbursed.

- There is no change in the value of other assets and liabilities. You are required to pass necessary journal entries on Charu’s admission.

Question 8

Mitesh, Samir and Ajay were partners sharing profits and losses in proportion to their capitals, which on 31st March, 2023, stood at: Mitesh - ₹ 1,50,000

Samir - ₹ 1,00,000

Ajay - ₹ 50,000

The firm’s recorded liabilities on that date amounted to ₹ 1,00,000. In addition:

- Ajay had given a loan of ₹ 40,000 to the firm on which he was entitled to receive interest @ 6% per annum for the whole year.

- A Bills Receivable of ₹ 40,000 discounted with the bank was dishonored on 31st March, 2023.

The partners dissolved their partnership firm on 31st March, 2023, and the assets, apart from cash of ₹ 30,000, realised ₹ 6,00,000. Expenses of dissolution amounting to ₹ 12,500 were to be borne by Samir. These were paid by the firm on his behalf.

You are required to prepare:

(i) Realisation Account.

(ii) Ajay’s Loan Account

For complete ISC Class 12 Accountancy Specimen Paper, click on the link below.

Keep tuning in to Jagran Josh for subject-wise ISC Class 12 Specimen Paper 2024. Also, keep reaching out to our website for any exam and education-related updates.

Also find:

ICSE, ISC Exam Pattern 2023-2024(PDF)

ISC Class 12 Specimen Papers 2023-2024(PDF)

ISC Class 12 Syllabus 2023-2024(PDF)

ICSE, ISC Syllabus 2023-2024(PDF)

Related:

ISC Class 12 Accountancy Syllabus 2023-2024(PDF)

ISC Class 12 Physical Education Specimen Paper 2023-2024(PDF)